- Sen. Minority Chuck Schumer, D-N.Y., on Monday called on President-elect Joe Biden to cancel up to $50,000 for student loan borrowers. He also said that Biden can cancel the debt without leaving borrowers liable for taxes.

- Under most circumstances, borrowers are subject to taxes if a creditor cancels, forgives or discharges a debt for less than the amount owed.

- Right now, there’s a handful of scenarios in which debt may be forgiven free of taxes – but this only applies in a narrow set of circumstances.

Senate Minority Leader Chuck Schumer, D-N.Y., has called on President-elect Joe Biden to forgive up to $50,000 for student loan borrowers.

"Ahead of the new administration, the four of us are calling on the president of the United States to take executive action to administratively cancel up to $50,000 of student loan debt, for federal student loan borrowers," Schumer said.

He spoke in New York City on Monday, where he was joined by New York Democratic Congressmen-elect Mondaire Jones, Ritchie Torres, and – via an iPad – Jamaal Bowman.

Though debt cancellation often carries a tax bill for the borrower, Schumer said Biden can help student loan borrowers avoid that.

"He can also make it such that when they do this, they have no tax liability," Schumer said.

Indeed, this fall the New York senator and Sen. Elizabeth Warren, D-Mass., introduced a resolution that calls for the next president to use executive authority to cancel student loan debt and prevent federal student loan borrowers from facing a tax bill.

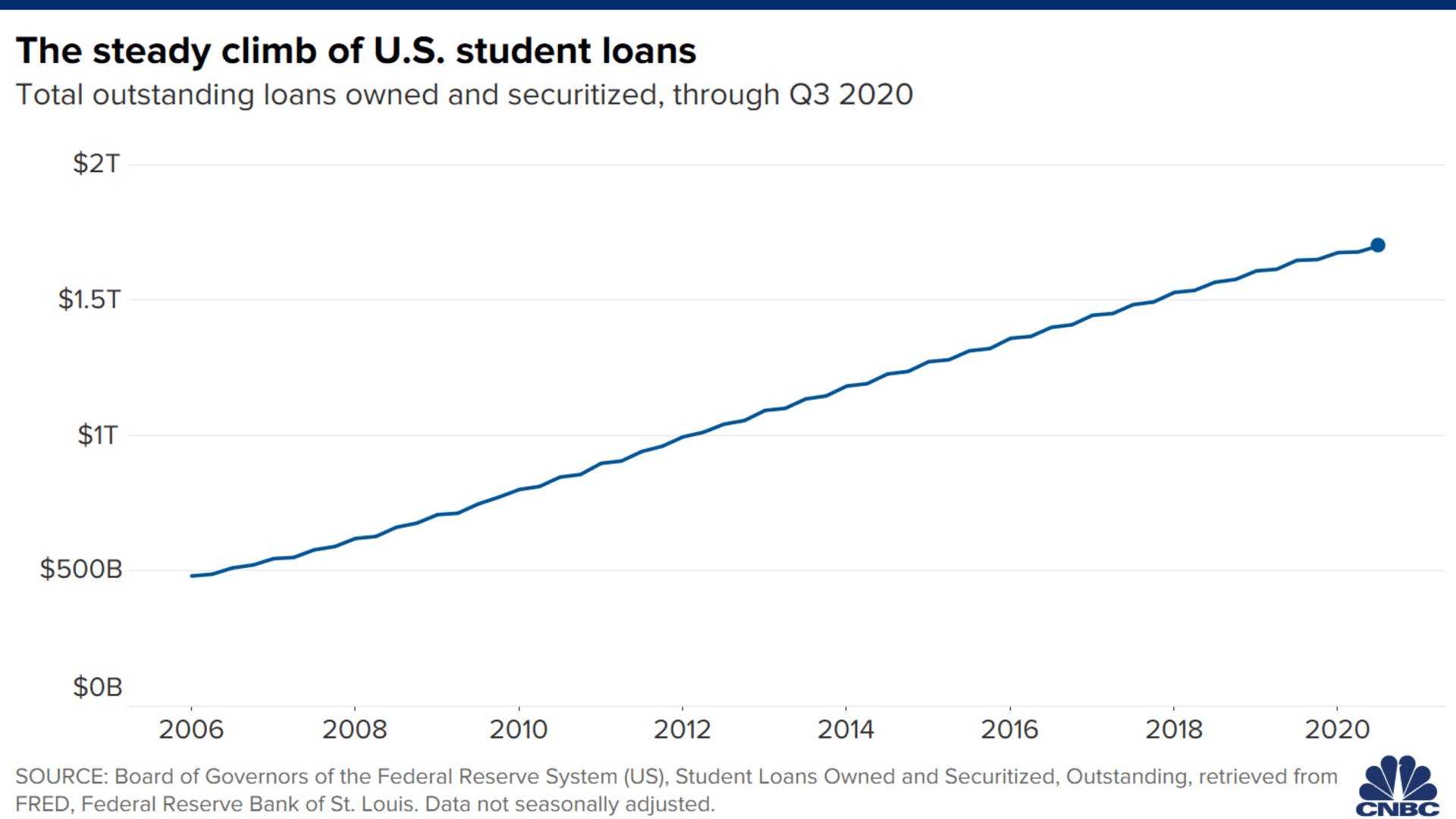

For cash-strapped households, wiping the debt would address the problem of monthly payments and a balance that continues to accrue interest.

Money Report

However, unless the tax issue is resolved, those borrowers would be on the hook with one of the toughest creditors around: The IRS.

"Once they do cancel the loans, does that cancellation of indebtedness trigger a tax bill?" asked John R. Brooks, professor of law at Georgetown University Law Center. "The knee-jerk tax lawyer answer is that if you cancel debt, then it's income unless you can point me to an exception."

"My point is that that simplistic view ignores a whole lot of other law and history relative to student debt," he said. "There are different paths to approach the problem and it will be interesting to see how they go."

Narrowly targeted relief

There are a few situations that allow for tax-free debt forgiveness under the current law.

First, there's the Public Service Loan Forgiveness program, wherein a borrower's remaining federal loan balance will be wiped after 120 qualifying monthly payments. Students must be working for the right kind of employer: a government organization or a 501(c)(3) not-for-profit.

The program is far from perfect. Nearly 180,000 unique borrowers have applied to have their debts wiped, and just 3,469 have been forgiven, according to September data from the U.S. Department of Education.

Debt forgiveness under the public service program is tax-free.

There's also the "insolvency exception" that's already written into the tax code.

"The insolvency exception from cancellation of debt income likely applies to many taxpayers with heavy outstanding loans from college and graduate school," said Joshua Blank, professor of law at the University of California, Irvine School of Law.

He gave the example of a taxpayer with $200,000 in student loan debt, plus $50,000 of other debt and $10,000 in cash in a bank account — her only asset. Under the "insolvency exception," this person would be insolvent by $240,000.

In this case, the person's student debt could be cancelled and excluded from her income. However, there's a trade-off: The insolvent taxpayer loses some "tax attributes" or certain tax benefits, which include her basis in property and net operating losses.

Student debt that's discharged due to death or total and permanent disability of the student is also tax-free.

Finally, back in January, the IRS and Treasury Department gave tax relief to defrauded students who had their balances wiped when their colleges closed.

Disaster relief amid Covid

For now, it remains to be seen how Congress or the new Biden administration will help student loan borrowers contend with taxes stemming from debt forgiveness.

A possibility could be for the forgiveness to be part of a Covid-19 stimulus program, said Brooks. Perhaps it could be deemed a "qualified disaster relief payment" that's excluded from gross income, he said.

Congress could also draft legislation that ensures only borrowers below a certain adjusted gross income receive tax-free forgiveness, said Leandra Lederman, director of the tax program at the Indiana University Maurer School of Law.

"You could do that here," she said. "Exclude from income up to $50,000 of cancellation of indebtedness if the adjusted gross income is under a certain level and then phase it out."

How Washington develops a solution for the taxes could come down to how they roll out the relief in the first place.

"There have been arguments back and forth that if this were done by executive order rather than through legislation, it's hard to see how that would not be subject to tax liability," said Kim Rueben, director of the State and Local Finance Initiative at the Urban-Brookings Tax Policy Center.

"If it's subject to tax liability, then it's really bad policy right now," she said. "The people who are going to do well are the ones who can afford the tax debt, but those who are struggling?"

"You're replacing student loan debt with owing the IRS, and it doesn't feel like a good exchange," Rueben said.