Anxiety and trauma sufferers are sometimes asked to define a hierarchy of fears that trigger distress so they might be managed.

An anxious Wall Street faces a litany of fears right now that have shadowed the broad market on its way to a near-20% decline into Thursday's urgent sell-off and remain after Friday's strong and perhaps overdue 2.4% bounce.

Nasdaq Y2K Crash Rerun?

Of course, the crucial real-world economic swing factor is whether the ongoing inflation, consumer malaise and financial-condition tightening represent the overture to a recession in coming quarters.

Get Tri-state area news and weather forecasts to your inbox. Sign up for NBC New York newsletters.

But from an investor's perspective, given the damage already done and the drivers of index performance and paper wealth, the top-ranked fear is that the Nasdaq tailspin is following the script from the post-peak bear market of 2000-2002.

Without having foretold the kind of rapid selling storm of recent months, I've noted here early this year that there are just enough parallels to keep the worry flowing: Years of tech-stock dominance, heavy market concentration among a handful of digital-economy winners, star fund managers who embodied "new era" thinking while disdaining traditional valuation methods.

And the cadence of the recent Nasdaq sell-off somewhat resembles the action after the March 2000 bubble top, a rapid 30% drop over a matter of months. The difference between a 25%-plus tumble in the Nasdaq being a great buying opportunity and just the start of the pain hinges entirely on whether the 2000-2002 rules apply.

Money Report

Bespoke Investment Group scanned all Nasdaq declines of 25% as well as 20% drops over 30 trading days. Both conditions apply to the present Nasdaq slide. Outside of periods beginning in the year 2000, every one of the drops led to hefty gains over the following year. The instances starting in 2000 – when the first 30% Nasdaq drop over a couple of months led to another 68% meltdown over more than two years – were a vicious trap for buyers.

And back then there were two classes of tech plays – the upstart speculative "story stocks," hundreds of which came public in 1999 alone, many with minimal or no revenue – and the anointed winners of the computing and networking age, which were profitable but quite highly valued. This somewhat mirrors today's divide between the unprofitable "disruptors" that peaked more than a year ago and the megaliths of the Nasdaq that came to be known as FAANMG.

Back then the flimsy, low-quality stocks imploded and then eventually even the high-quality winners succumbed. Microsoft — then as now one of the two largest companies in the market — fell more than 60% in the 2000-'02 bear market. Cisco collapsed 90% and even reliable old Hewlett-Packard shed more than 80%.

This is where the significant differences between now and two decades ago come in to offset some of the worst fears.

There was vastly more air under the Nasdaq Composite at its March 2000 peak. It had gained more than 500% over the prior five years, compared to 200% over the five years leading up to the most recent Nasdaq record about six months ago. So ferocious was the momentum rush into early 2000 that the Nasdaq reached a fuselage-shaking 55% above its 200-day moving average; at last November's top this spread was 12%.

And to illustrate the gulf in valuations now versus then, Microsoft at the 2000 peak traded for more than 60-times forecast earnings and would fall to 22-times by the 2002 tech-sector trough. Its multiple peaked this cycle around 35 and is already down near 24.

In fact, the Nasdaq of the late-'90s was made up generally of less-mature, more volatile and frothier stocks than today, when its five largest companies are also the top five in the overall U.S. market.

The Nasdaq of 2000 more resembles the ARK Innovation fund (ARKK) in this regard, a higher-octane, riskier segment of the market. And the price action there has matched that of the old Nasdaq bust pretty well, as Chris Verrone of Strategas Research has been tracking. In fact, ARK has overshot the Nasdaq collapse to date, suggesting perhaps that most of the reckoning in speculative tech might have run its course.

Hot Powell Summer

Investors are now six months removed from the start of the Federal Reserve's sharp swerve toward a more hawkish outlook for lifting interest rates and bleeding down its balance sheet.

Yet Chair Jerome Powell's resolve in conveying his inflation-fighting intentions and implicit acknowledgement that an "economic soft landing" is more aspiration than expectation continues to hover as a primary fear weighing on investor risk appetites.

Expectations of half-percentage-point rate hikes each in June and July and perhaps September are now reflected in the economic consensus and, largely, in bond prices. Last week, Powell's comments in an interview that he never intended this month to foreclose on the chance or a 0.75% hike didn't seem to unnerve bond traders, indicating general agreement about the policy path through summer.

Yet because this path seems not to be subject to much change even if inflation data start to recede faster, it leaves investors with a sense that risk assets are capped (if not harshly handicapped from here) as the Fed seeks to ratchet financial conditions tighter.

This psychological (and financial) overhang joins with the general awareness that mid-term election years have tended to be choppy and sloppy through summer and concern that corporate earnings forecasts are vulnerable to cuts.

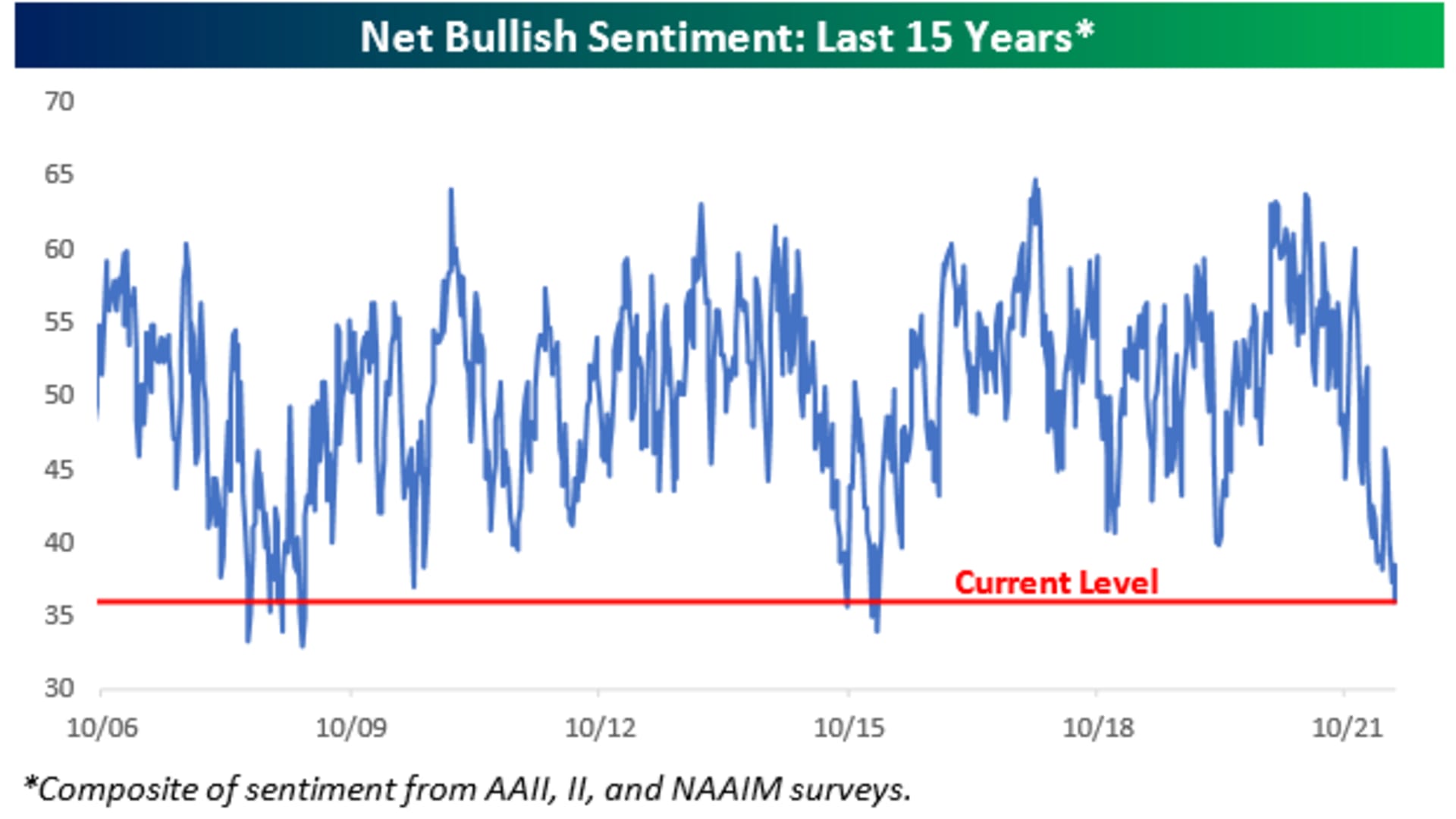

Of course, low expectations are not a bad starting point for markets. At last week's lows, sentiment began to register pessimistic extremes, and over a time frame of months or more this starts to have favorable implications for equity performance.

Still, the phrase "Don't fight the Fed' became a cliché for a reason, so bounces and feints in the indexes should be expected.

Accident Patrol

Cryptocurrency prices in freefall, synthetic "stablecoins" coming unstuck, signs of urgent liquidation in big tech stocks, acutely poor trading liquidity in equities and bank shares in a deep skid leave plenty of room for anxiety over potential financial mishaps.

This is a mostly free-floating "What if?" factor that befogs the markets during corrections, perhaps exacerbated now by the sense that the bar is high for the Fed to rescue asset owners in the event of a rupture.

So far there are no real alarms sounding in the capital markets. The spread above Treasuries now demanded by junk-debt owners is on the rise but not bumping against panic levels yet, but the direction of travel is uncomfortable. No reason for fright, but credit conditions remain in the hierarchy of fears.

These issues will probably retain their power to spark scares in a twitchy market. Though in the near term, the stock market seems governed by the tactical playbook around corrections: oversold readings, short-covering and rally attempts requiring close scrutiny to gauge their staying power.

Last week, this column detailed a confluence of downside S&P 500 targets between 3800-3900 based on a variety of technical, fundamental and history-minded approaches. That zone was tested in a hurry, Thursday's low coming just above 3850.

The bounce from there from oversold levels with the S&P 500 just shy of the minus-20% threshold and with the Nasdaq 100 having shed almost exactly half of its post-March 2020 rally was intuitive, welcome and relatively impressive – both satisfied bears and wishful bulls concluding the tape had suffered enough for now.

Sure, the most devastated stocks rebounded hardest, the Goldman Sachs non-profitable tech-company basket up 12% Friday yet still off 50% this year. Short covering was rife, but it always is from the correction depth, and 90% of NYSE volume was to the upside, which lends it some credence.

The S&P was pulled so taut that handicappers were willing to grant that it could rise, say, another 7% from here without even threatening the entrenched downtrend. If the rally is able to burn up more of the fear to run that far, it will have done so in the face of looming fears that won't soon dissipate but perhaps now can be named and managed.