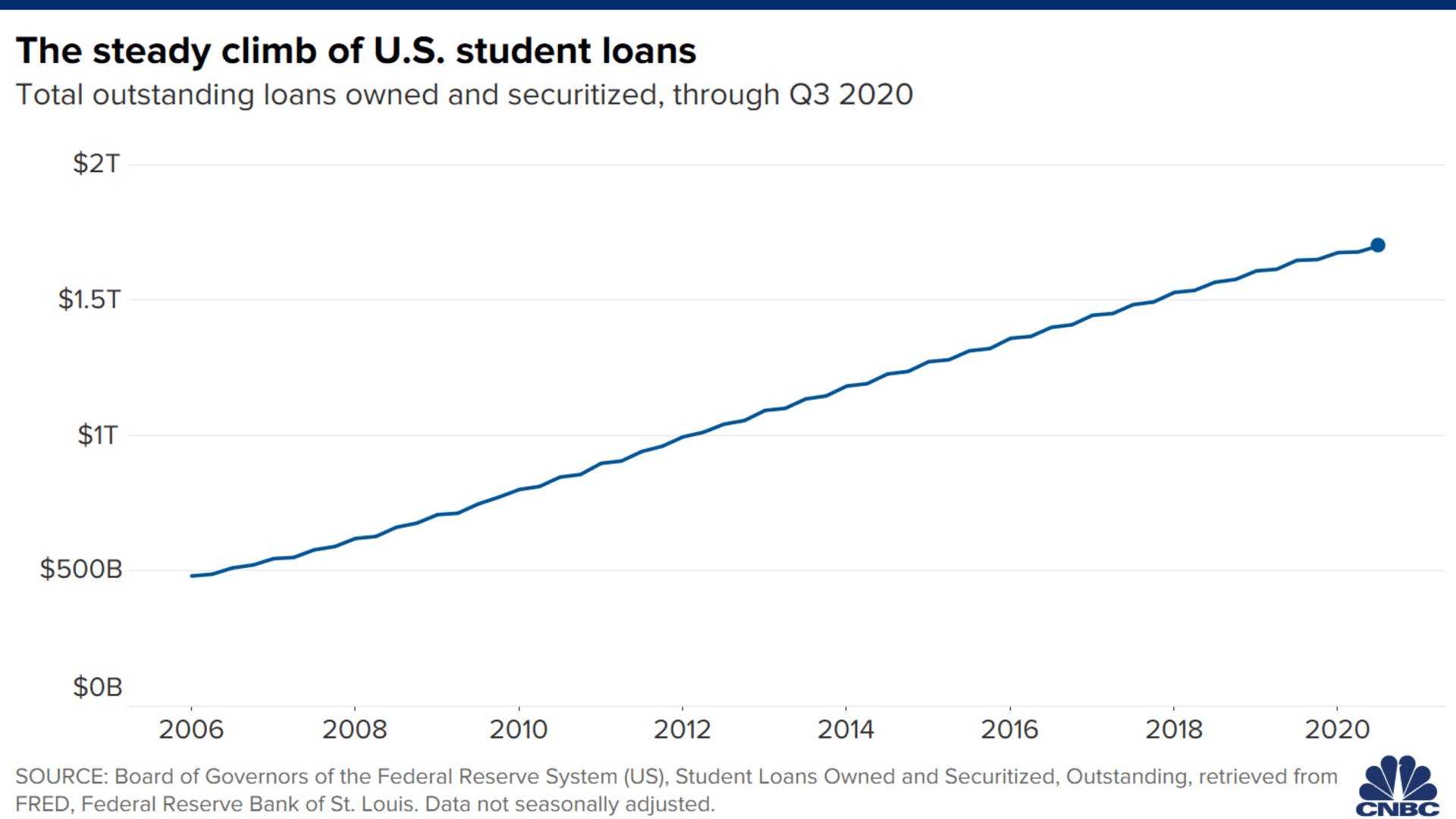

- Student loan borrowers have been hoping for news of forgiveness.

- Instead, they're getting reminders from their servicers that the bills will soon resume.

- As a result, they should take these these steps to get ready, experts say.

With attention in Congress on infrastructure and a new budget, discussions about student loan cancellation seem to be on the shelf.

And despite the pressure some Democrats have put on President Joseph Biden to wipe out the debt through executive action, he has expressed mostly hesitancy about doing so.

As a result, higher education expert Mark Kantrowitz said: "Borrowers shouldn't bank on forgiveness."

Get Tri-state area news and weather forecasts to your inbox. Sign up for NBC New York newsletters.

What they can expect are their monthly bills to soon resume. Since March 2020, the U.S. Department of Education has given borrowers the option of pausing their payments without interest accruing, but that break will end in January.

Here's how to get ready for repayment, in case the jubilee doesn't occur for awhile, or, ever.

When will bills be due again?

Money Report

The pause is scheduled to end on Jan. 31, 2022.

That means most borrowers will have their first payment due again sometime in February, depending on the date they began paying their loans.

Although the payment pause has been extended repeatedly during the pandemic, don't expect that to happen again. When the White House announced its most recent extension last month, it said that it would be the final one.

What if I can't afford to start paying again?

If you're still unemployed or dealing with another financial hardship because of the pandemic, you'll have options come February.

First, put in a request for the economic hardship or the unemployment deferment, experts say. Those are the ideal ways to postpone your payments because interest doesn't accrue under them.

If you don't qualify for either, though, you can use a forbearance to continue suspending your bills. But keep in mind that interest will rack up and your balance will be larger (sometimes much larger) when you resume paying.

If you expect your struggles to persist, it may make sense to enroll in an income-driven repayment plan. These programs aim to make borrowers' payments more affordable by capping their monthly bills at a percentage of their discretionary income and forgiving any of their remaining debt after 20 years or 25 years.

How do I decide on the right payment plan?

Many people's lives have been changed by the pandemic.

If your circumstances look different than before March 2020, it may make sense to review the payment plans available to you and find one that's the best fit for your current situation.

In the meantime, the law has also changed.

Student loan forgiveness is now tax-free until at least 2025, thanks to a provision included in the $1.9 trillion federal coronavirus stimulus package signed into law in March. The policy will likely become permanent.

That may make income-driven repayment plans more appealing, since they often come with lower monthly bills and borrowers will likely no longer be hit with a massive tax bill at the end of their 20 years or 25 years of payments.

But if you can afford it, the standard repayment plan is just 10 years.

To calculate how much your monthly bill would be under different plans, use one of the calculators at Studentaid.gov or Freestudentloanadvice.org, said Betsy Mayotte, president of The Institute of Student Loan Advisors, a nonprofit.

If you do decide to change your repayment plan, Mayotte recommends submitting that application to your servicer sooner rather than later.

"I have significant concerns that there will be some big servicing delays," Mayotte said.

What should I do now?

Over the next four months, borrowers should make sure that their student loan servicer has their current contact information, Kantrowitz said. If you've moved, for example, they may not.

If you were enrolled in automatic payments and your banking information has changed, you'll also want to notify your servicer of that.

Putting aside some money for when payments begin again may also make the transition less painful, experts say.

Is student loan forgiveness still possible?

Biden has asked the U.S. Department of Justice and the U.S. Department of Education to review his legal authority to forgive student debt through executive action. The fact that those reports are still pending may explain why we haven't heard anything more definitive yet, experts say.

"He's not going to take any steps until that report comes back," Kantrowitz said.

However, borrowers may see action before February, he said.

"You wouldn't want to restart payment on some borrowers' student loans, only to forgive them a month or two later," Kantrowitz said.

The White House did not immediately respond to a request for comment.

Should I think about refinancing my student loans?

Borrowers thinking about refinancing their federal student loans into private loans for a lower interest rate may want to wait, Kantrowitz said. For one, the interest rate on most federal student loans is 0% for another four months.

What's more, "they will feel foolish if they refinance only to have the federal government announce loan forgiveness," Kantrowitz said.

What should I do with extra cash in the meantime?

The typical student loan payment is around $400 a month.

While the bills are on pause, experts recommend using the additional money in your budget to beef up your emergency savings and pay down credit card debt.

People should try to build up at least six months' worth of expenses in cash should they have to live through a period of unemployment, experts say.

To get the best return on your cash, keep your money in a high-yield savings account. It's worth shopping around with different banks to find the best offer. The average online savings account rate is 0.45%, while it's just 0.13% with traditional brick-and-mortar banks and credit unions, according to DepositAccounts.com.

"It may not seem like much, but $100,000 earning 0.50% is $500 a year," aid Allan Roth, founder of financial advisory firm Wealth Logic in Colorado Springs, Colorado.

You'll just want to make sure any account you put your savings in is FDIC-insured, meaning up to $250,000 of your deposit is protected from loss.

If you have an adequate cash cushion, knocking down credit card debt can save you a lot of money.

Ted Rosman, an industry analyst at Creditcards.com, provided an example. If you're carrying $5,500 in credit card debt and make only the minimum payments each month, you'll be stuck paying for more than 16 years and shell out an extra $6,163 just in interest, assuming you're getting dinged the average annual fee of over 16%.

If you dedicate an extra $400 per month for just the next four to that balance, however, it'll trim almost three years off that schedule — and you'll save $2,162 in interest by doing so.